Managing a high-growth financial institution in the Sunbelt requires navigating a unique economic paradox. While the region’s commercial development remains highly dynamic, the volatility of interest rates has placed loan portfolios under unprecedented pressure. For dominant regional banks this reality hits close to home due to an exceptionally high exposure to Commercial Real Estate (CRE) in Florida.

In this market environment, credit risk is no longer a metric you can afford to evaluate in hindsight. Traditional reporting models that rely on static data leave roles like the Chief Risk Officer (CRO) facing a significant visibility gap.

To protect the balance sheet, regional leaders must transition from backward-looking compliance reporting to forward-looking risk intelligence, using dynamic executive dashboards to capture portfolio stress before assets begin to deteriorate.

Why are traditional quarterly reports a bottleneck for commercial real estate credit risk solutions?

The short answer is latency. When credit risk teams rely on retrospective summaries, they are essentially steering a high-exposure ship by looking at the wake. Traditional quarterly reviews only show the financial health of a borrower or a property after a payment cycle has been missed or a covenant has been breached. By then, capital drain has already begun, and mitigation options are limited.

Implementing modern commercial real estate credit risk solutions requires breaking free from the constraints of legacy batch processing. While building an integrated data layer is the architectural foundation for CRE risk management analytics, the true strategic value for the C-suite lies in real-time execution. When macroeconomic indicators shift rapidly, waiting 90 days for a portfolio review creates an architectural bottleneck that exposes the bank to unmitigated market friction.

How does real-time portfolio stress testing for banks enable preventive credit decisions?

The alternative to reactive reporting is the deployment of an interactive, predictive dashboard designed for advanced decision support. Rather than acting as a passive display, this predictive dashboard functions as an active advisory tool that continuously tracks portfolio metrics, automatically triggers early-warning alerts, and suggests strategic mitigation steps before credit quality deteriorates.

By feeding continuous data streams into localized risk models, real-time portfolio stress testing for banks allows executive leadership to run dynamic, instantaneous simulations. The true power of this solution lies in its total data versatility; it is completely agnostic to the underlying infrastructure, meaning it seamlessly integrates and harmonizes data from any legacy core, modern CRM, or third-party market feed without friction.

Instead of reading a static PDF, a CRO can actively manipulate risk variables on a digital canvas to visualize immediate impacts on the portfolio:

- Proactive Exception Handling & Tiered Alerts: Setting automated, multi-level alerts based on strict business rules to flag early indicators of deterioration, such as sudden drops in tenant-level cash flows. The system instantly routes these notifications through preferred corporate channels (SMS, Email, or Teams) directly to the specific risk officers or asset managers responsible, allowing them to restructure terms preventively before a major breach occurs.

- Interest Rate Shocks: Instantly mapping which CRE loans in South Florida will drop below acceptable Debt Service Coverage Ratios (DSCR) if variable rates fluctuate another 50 basis points.

- Granular Occupancy Declines: Simulating localized stress scenarios, such as a localized retail downturn, to identify vulnerable concentration risks before they trigger a downgrade.

This level of visibility transforms risk management from a secondary defense mechanism into a high-velocity engine for capital preservation.

Driving operational resilience through predictive credit risk analytics in banking

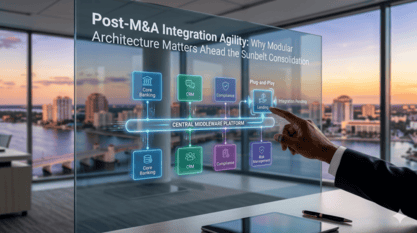

Deploying executive dashboards does not require a disruptive, multi-million-dollar replacement of your core system. Instead, it relies on an agile middleware layer capable of orchestrating data flows from fragmented workflows and third-party market data.

This integration philosophy is exactly what drives post-M&A integration agility during active consolidation, ensuring that newly acquired loan books are instantly visible under the bank’s risk umbrella.

By leveraging predictive credit risk analytics in banking, regional leaders can bridge the gap between IT infrastructure and financial performance. This approach directly aligns with the objectives of banking operational automation, where the ultimate goal is to eliminate manual data aggregation so that human talent can focus exclusively on strategic decision-making.

The Power of Preventative Analytics

At Pragma, we specialize in helping regional financial leaders build the high-performance data layers necessary to power advanced risk intelligence. Our implementation frameworks allow institutions to:

- Consolidate fragmented data portfolios into unified, single-source-of-truth executive dashboards.

- Embed intelligent workflow automation that reduces data latency, allowing risk indicators to update in real time rather than at month-end.

- Apply AI-driven classification models to automate high-volume compliance and portfolio monitoring, mimicking the frameworks used to automate risk management with intelligent architectures.

In the current banking landscape, capital resilience is dictated by speed. Transitioning to real-time risk intelligence ensures that your institution doesn't just measure risk, but actively outmaneuvers it.

Is your portfolio equipped for real-time visibility?

Request a custom Data & Risk Assessment now!