For growing financial institutions, operational scale often creates a paradox: the institution wins more business, expands its portfolio, or enters new markets, but every new loan, exception, compliance review, or approval path adds pressure to teams already working across fragmented systems. Across the banking industry, innovation is increasingly being measured by execution: whether institutions can improve speed, control, and scalability in the operating model.

When volume increases, the Efficiency Ratio, a key performance metric for leadership teams and boards, often deteriorates due to middle-office friction. To compete more effectively, banking leaders must transition from labor-intensive processes to scalable architecture.

True operational resilience relies on modernizing these foundational workflows; by implementing middle office automation in banking, institutions can drive sustainable operational leverage, enhance internal auditability, and turn the commercial loan process into a controlled framework for long-term competitive execution.

In banking, the middle office is where critical operational work happens between customer-facing teams and core systems: document intake, data validation, compliance checks, risk review, underwriting support, exception handling, and internal approvals.

Why middle office automation matters for operational efficiency?

Traditional models for scaling banking operations face diminishing returns under modern market pressures. Historically, expanding a commercial loan portfolio required a linear expansion of back and middle-office staff to manage data extraction, compliance verification, and underwriting queues.

As discussed during recent Florida Bankers Association (FBA) panels, automation only creates value when it addresses the underlying workflow design. Simply automating a fragmented or inefficient process does not resolve the structural bottleneck; it merely accelerates it.

True banking efficiency ratio solutions require a deep structural decoupling of asset growth from operational expense. By integrating automated checkpoints directly over legacy infrastructures, institutions can reduce manual screen-switching for analysts. This technical optimization shields the bank’s operating margin from post-M&A labor overhead, allowing institutions to absorb higher volumes without increasing operational headcount at the same pace as business growth.

Scaling commercial loan workflow automation with speed and control

In commercial lending, velocity is an important driver of customer retention. Larger institutions can face bureaucratic complexity, leaving visibility gaps during credit approvals. Implementing workflow automation for commercial loans allows regional banks to transform this pain point into a competitive advantage.

By deploying specialized, governed automation agents that support middle-office teams, institutions can compress repeatable validation and review steps from weeks to hours in targeted use cases, without removing the human judgment required for risk and credit decisions.

Crucially, as we explored in our analysis of CRE risk management analytics, middle-office velocity only creates value when it remains connected to portfolio visibility, risk controls, and governance. Accelerating commercial loan workflows should never come at the expense of sound credit discipline; it should strengthen the quality, traceability, and timeliness of the information used for risk decisions.

Where automation creates operational leverage

Optimizing your commercial loan disbursement time changes how high-value business clients perceive your brand:

- Instant Verification Loops: Underwriting data fields auto-populate directly from customer uploads into your core systems via secure API orchestration layers.

- Programmable Compliance Checks: Rule-based verification engines validate entity data in real-time, reducing avoidable manual routing delays.

- Tiered Exception Routing: Clean files can move through predefined approval paths, while complex anomalies are escalated to senior risk officers.

This technical agility enables teams to respond faster, improve process visibility, and strengthen the customer experience without compromising control.

Driving lean growth through tailored banking efficiency ratio solutions

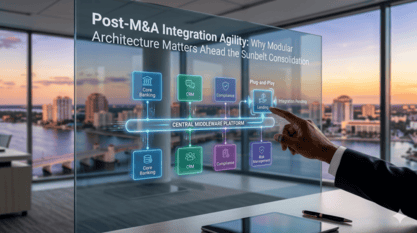

Moving your institution toward a modern, automated operating model does not mean assuming the system-wide risk of a total core "rip-and-replace" modernization. Modern banking technology has evolved to utilize intelligent middleware layers that sit securely above your current systems of record. This approach directly reinforces post-M&A integration agility, helping newly integrated teams align more quickly with centralized operating standards.

The goal is not only to automate tasks, but to create an operating model where growth does not automatically translate into more manual work. At Pragma, we help financial institutions design and build automation architectures that connect existing systems, orchestrate workflows, improve traceability, and support scalable execution.

By optimizing workflows and reducing repetitive data entry, institutions can achieve higher straight-through processing rates, minimize manual touches, and improve their transactional banking operational automation cost-to-serve metrics. This structural framework ensures that your technology infrastructure actively amplifies your strategic goals, allowing you to maximize the value of your human capital without leaking profitability.

The institutions that scale most effectively will be the ones that redesign operational workflows to improve speed, control, visibility, and consistency. Is your middle office optimized for scalable growth?

Start with a focused operational efficiency assessment to identify where automation can reduce manual work, improve traceability, and support scalable growth.

Request an operational efficiency assessment